#029 - Klarna

Klarna - Private

Klarna is a European based BNPL competitor. Klarna processed the most GMV of any competitor in this industry. Klarna recently raised more than $600 million at a valuation north of $45 billion.

If you want to become a paid subscriber sign up below!

The monthly subscription is $7. Although I’ve created a paid subscription, I’m keeping all my writing open to the public. I refuse to put anything behind a paywall. My hope is that enough people will become a paid subscriber to support this project. One benefit of being a paid subscriber is being able to vote on the industries that I cover in my research.

Please note that this article does not constitute investment advice in any form. This article is not a research report and is not intended to serve as the basis for any investment decision. All investments involve risk and the past performance of a security or financial product does not guarantee future returns. Investors have to conduct their own research before conducting any transaction. There is always the risk of losing parts or all of your money when you invest in securities or other financial products.

Industry Overview

Klarna competes in the BNPL space with other competitors like Affirm, Afterpay, Quadpay (recently acquired by Zip), PayPal, and a handful of other smaller competitors. Much of my original thoughts on the BNPL industry can be found via my shallow dives on Affirm and Afterpay.

Klarna is the last BNPL company that I will be covering in this newsletter. There are a number of other companies, but these companies aren’t a true BNPL company and do much more than just BNPL. Researching Affirm, Afterpay, and now Klarna has given me a good starting point on this industry and hopefully it has also given you a good starting point. Of course, my research isn’t meant to be a full deep dive on companies, but more of an introduction and you can decide where to go from here.

One important point I want to note is that I believe this industry will eventually turn into an oligopoly with only a handful of competitors. This will likely make this an attractive industry to search for opportunities among the handful of scaled competitors. I believe there are high barriers to entry and these companies will have strong competitive advantages which will prevent this industry from becoming commoditized with little to no profit pool.

Business Overview

Klarna is a BNPL competitor based in Europe and headquartered in Sweden. Klarna was founded by Sebastian Siemiatkowski, Niklas Adalberth, and Victor Jacobsson in Stockholm back in 2005. Affirm and Afterpay were founded in 2012 and 2014, respectively. This has given Klarna a head start on its competitors.

Klarna’s business model is more similar to Affirm than Afterpay. Klarna makes revenue three ways. Klarna receives a commission from merchants, receives late fees from consumers, or receives interest from customers. Afterpay doesn’t charge interest but also doesn’t finance more expensive purchases like a new Peloton bike. Affirm and Klarna allow consumers to finance larger purchases but these purchases come with interest payments.

Klarna has historically focused on Europe and has been expanding into other regions like the US, China, and other regions. So far Klarna has done a good job of expanding into the US and abroad. For example, I’ll list a number of screenshots below that help give a better description of Klarna’s expansion. The first screenshot represents Klarna’s global app installs in 2020 compared to 2019 and also compared to other competitors in 2020.

The next screenshot below represents Klarna’s US app installs in both 2019 and 2020 and compared to its closest competitor (likely Afterpay?). This is a good sign for Klarna as it’s growing its consumer base quite rapidly, but this needs to come with growth in merchants.

While the two screenshots above are biased in favor of Klarna (from Klarna’s annual report), comparing the GMV of the top three competitors (Klarna, Afterpay, and Affirm) might give a better idea of what company has the largest scale.

Klarna is the largest BNPL competitor by GMV. Klarna processed ~$53 billion in GMV in 2020. Afterpay processed ~$9.8 billion and Affirm processed ~$4.6 billion. Klarna processed more than 5x and 11x GMV than its closest competitors, respectively.

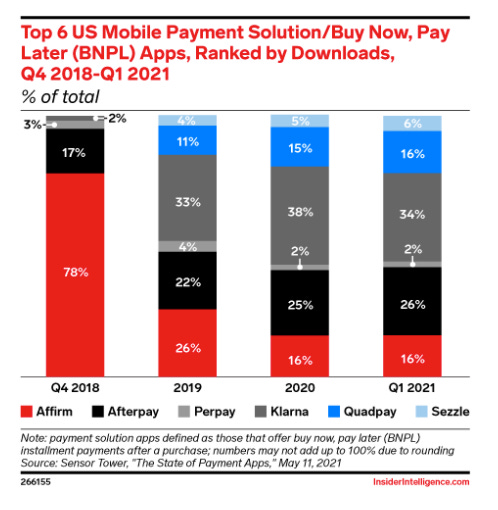

Another screenshot below shows US downloads for BNPL apps over time from Q4 2018 to Q1 2021. Klarna made a significant jump from ~3% to 33% in 2019, but has since stagnated through Q1 2021 while Afterpay and other apps have grown in popularity. One interesting point is the drop in Affirm’s US market share as other competitors have started to expand into the US.

Total Addressable Market

Like I’ve mentioned before BNPL competitors are competing in the retail market and their total addressable markets are a percentage of the total GMV spent by consumers likely worldwide or including consumers of most companies plus interest revenue plus any future optionality in these businesses (marketplace, lending, etc).

The US retail market (online + offline) is worth ~$5 trillion. BNPL companies typically take up to 6% in commissions from merchants for helping merchants sell products and services. For simple math, we’ll say the total addressable market for US alone is worth ~$250 billion (5% of $5 trillion). While this number is split between cash, credit cards, debit cards, and now BNPL services, this is a massive market for Affirm, Klarna, and Afterpay.

There is room for expansion in international markets as well. The $5 trillion market is only US retail and does not include international opportunities like Europe, Asia, South America, or elsewhere.

There was a quote in Klarna’s annual report that I thought was interesting and spoke to the potential for Klarna and this market:

“Global retailers want global partners”

While there might be local winners such as Afterpay in Australia or Klarna in Europe, large retailers (like Nike, Lululemon, and others) want to work with 1 or 2 companies, not 100s. Of course, to play devil’s advocate, a consumer will be local not global. Consumers will use whatever the traditional BNPL offering is in a specific region.

Competitive Advantages

Scale

One aspect of this industry that will lead to high barriers to entry is the amount of data needed to minimize credit losses while still having customers. By the time competitors might try and displace the top BNPL companies, Klarna, Affirm, and Afterpay will likely have years worth of data and consumer behavior to minimize risk and maximize profits.

Smaller competitors will likely stand no chance against these incumbents without millions of dollars to market to customers (not impossible with VC money) or a better product for both merchants and consumers.

Small but powerful network effects

I’ve touched on this before but will repeat again. Consumers will use BNPL solutions that are taken by the majority of retailers. Retailers want to work with BNPL companies that have a large user base. This creates a network effect. More consumers leads to more retailers. More retailers lead to more consumers. And the cycle repeats itself.

While the top competitors have built this network of merchants and consumers (and might be commoditized among the top competitors), smaller competitors and any future competitors will have to replicate this network effect in order to be competitive. That will likely be tricky to replicate because consumers and merchants don’t want to adopt another solution if it’s only marginally better than their current solution.

Switching costs

As consumers’ habits grow and become stable, these users won’t switch to other solutions for a 10% improvement. These BNPL companies want to do more than just finance purchases for consumers. Afterpay wants to be a quasi marketplace, Affirm wants to get into banking, and Klarna likely wants to get into banking, lending, become a quasi marketplace, a mix of all three, or more!

As these top companies grow and expand into other financial service offerings consumers are going to become more trapped in this ecosystem and competitors won’t be able to target these consumers.

Financials

All figures below are in USD and are roughly accurate. I used average exchange rates provided in Klarna’s annual report. Klarna is still a private company, so there is only so much information provided in its annual reports. Klarna was recently in some headlines because it raised ~$639 million at a valuation north of $45 billion.

2020

GMV = 53 billion

Net interest revenue = 289.5 million

Net commission revenue = 771.6 million

Total revenue = 1,087.0 million

Gross profit = 690.5 million

Total revenue as a % of GMV = 2.1%

GMV growth = 45.8%

Net interest revenue growth = 9.8%

Net commission revenue growth = 49.2%

Total revenue growth = 39.8%

Gross profit margin = 63.5%

2019

GMV = 35 billion

Net interest revenue = 255.4 million

Net commission revenue = 500.6 million

Total revenue = 753.1 million

Gross profit = 511.1 million

Total revenue as a % of GMV = 2.2%

Net interest revenue growth = 36.6%

Net commission revenue growth = 70.3%

Total revenue growth = 40.5%

Gross profit margin = 67.9%

It’s quite impressive that Klarna had north of $1 billion in revenue and is growing total revenue by close to 40% y/y.

What’s Interesting

BNPL = customer acquisition tool

One interesting idea that I’ve been thinking about with this industry is that BNPL services seems like a pretty compelling customer acquisition tool especially if these companies are moving into higher value services like banking, lending, or building a marketplace.

While BNPL companies will likely have strong operating margins at maturity, there is also the ability to cheaply acquire customers and then offer them higher value services in order to grow profit and have even better margins.

Largest competitor

Klarna just dwarfs other competitors in this industry. As Klarna grows, it continues to benefit from scale. Klarna can build out more financial offerings, invest in more brand marketing, and continue to grow its network of consumers and merchants. One characteristic I also look for is investing in the winners of an industry and Klarna seems to be a winner based on its large GMV and quick success in the US.

Future Questions

Paypal and other competitors?

While this will be my last shallow dive on the companies in the BNPL space, there are still a handful of other companies that are competitors. Paypal is a big incumbent. Paypal is just a big company that can’t be written about within a week. While BNPL might not be Paypal’s biggest priority, Paypal can throw its weight around to crush smaller startups.

There are still a number of smaller competitors like Quadpay (acquired by Zip co) and Sezzle (traded as ASX:SZL). These competitors might make it into the top handful of competitors if this industry turns into an oligopoly. More research will likely tell you this answer.

Optionality within Klarna?

One aspect of companies that I like to invest in are whether or not there is any optionality within the businesses and whether that optionality is priced in. While Klarna is yet to be public, the size of the business will likely be north of $50 billion when it does go public. Klarna recently raised ~$639 million at a post-money valuation of $45.6 billion. This makes it the second most valuable fintech startup in the world (only behind Stripe).

At the price of $45.6 billion, the chance of a 4x, 5x, or even 10x seems quite small, but this market is also quite large and Klarna has had great success thus far. The financial services industry is a big market with high customer lifetime value. If Klarna can expand into other services, the price might not be terrible.

Conclusion

I’ve enjoyed learning about this industry. I came into industry quite skeptical and wasn’t really sure how these were good companies or even would be good investments, but this is a good industry and I’m looking to learning more as these companies grow into the spotlight and become more ingrained in our society.

I’m mostly looking forward to Klarna going public, reading some more public filings, and seeing what revenue multiple they command.

If you’ve enjoyed this edition of Weekly 10-K please considering becoming a paid subscriber, sharing it with friends and colleagues, and following me on Twitter.