#027 - Affirm

#027 - Affirm

Affirm helps reduce the friction in purchasing products.

Affirm - (NASDAQ: AFRM)

Affirm is one of the major BNPL companies and is led by Max Levchin (one of the co-founders of Paypal). Affirm has seen tremendous growth in 2020 and is hopeful for strong growth moving forward as the economy reopens.

If you enjoy this, sign up for more shallow dives here!

Please note that this article does not constitute investment advice in any form. This article is not a research report and is not intended to serve as the basis for any investment decision. All investments involve risk and the past performance of a security or financial product does not guarantee future returns. Investors have to conduct their own research before conducting any transaction. There is always the risk of losing parts or all of your money when you invest in securities or other financial products.

Industry Overview

What is BNPL?

BNPL stands for buy now, pay later (BNPL). The name is self-explanatory, but BNPL helps consumers split up purchases over various periods of time. The most common length of time is 4 payments in six weeks (“Pay in 4”):

At purchase

2 weeks after initial purchase

4 weeks after initial purchase

6 weeks after initial purchase

Why BNPL?

Consumers don’t like opaque credit card fees and high rates of interest. Consumers want to be able to split up expensive purchases over a number of periods without accruing interest on their credit card. These BNPL competitors offer consumers a clear value proposition. Split up and delay payments, know exactly what you owe, and pay less fees because some costs are paid by merchants. Merchants like offering BNPL products because it increases conversion rate, average order value (AoV), and reduces friction in the transaction process.

Many of these BNPL competitors are taking on the credit card industry. They want to make the industry more transparent and improve how consumers see these types of companies.

Competitors

There are a number of competitors in this market. Affirm is the first company I’m doing a shallow dive on, but some other notable companies are Paypal, Klarna, and Afterpay.

One of the main factors that Affirm’s management touts as being different from competitors is that Affirm offers more flexible payment plans. Affirm’s competitors mainly seem to offer “Pay in 4” which splits payments into four equal payments (highlighted above). While the majority of Affirm’s payment plans span from 3 through 12 months, Affirm’s plans range from 6 weeks to 48 months. Why does this matter? Well if you have an expensive purchase, you don’t want the full amount sitting on your credit card, accruing interest, and affecting your credit score, so you choose to use a BNPL provider and split up those payments over a certain period of time.

Business Overview

Affirm is one of the major buy now, pay later (BNPL) companies, alongside Klarna and Afterpay. I addressed some of the key industry points above.

Affirm was founded by Max Levchin in 2012. Max Levchin was a co-founder of Paypal and is part of the “Paypal Mafia.” From an initial glance, Max seems like an incredible founder and his background seems to be well-suited to lead Affirm moving forward and building out more fintech products.

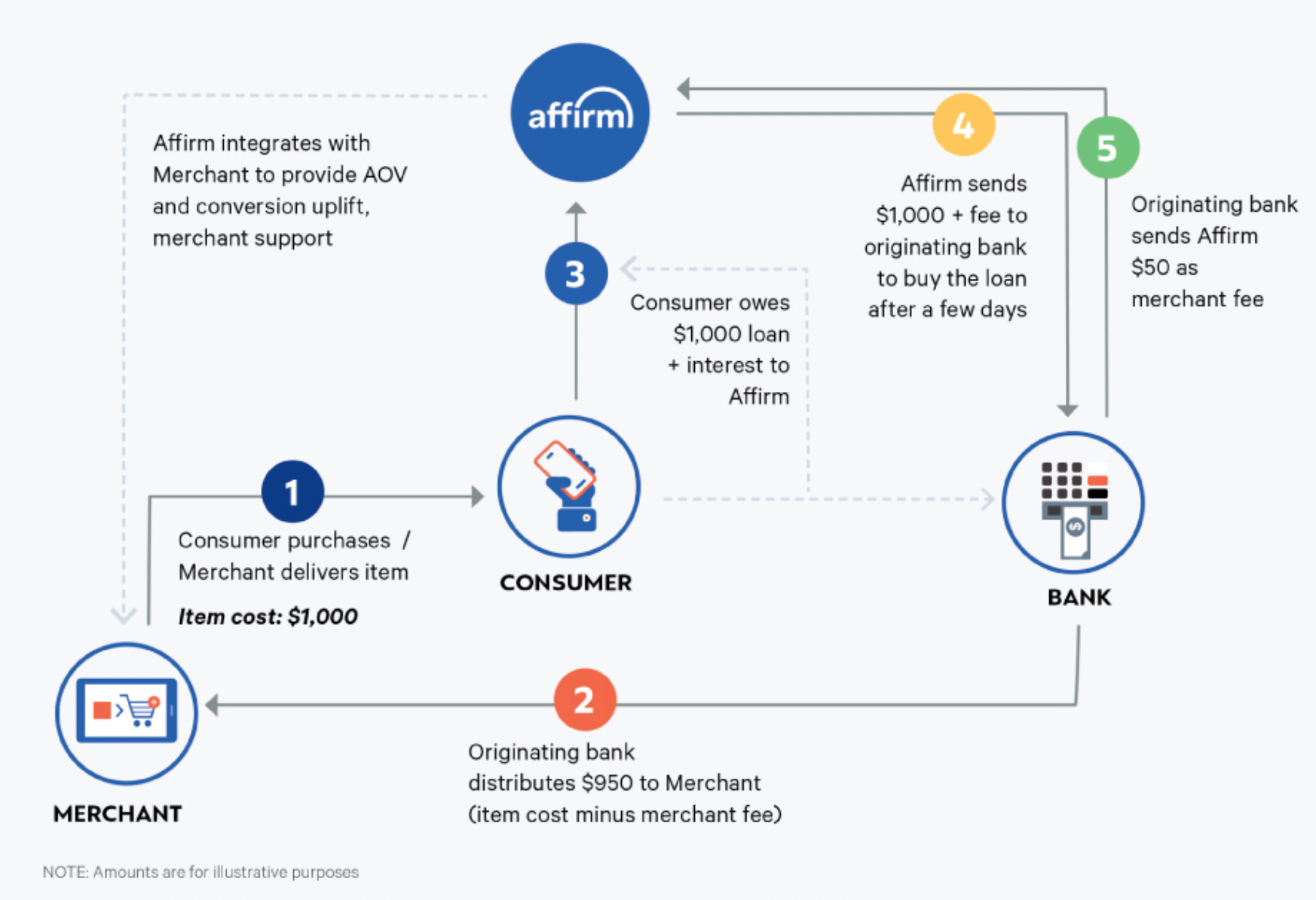

The graphic below gives a quick overview of an average transaction for Affirm and other parties:

Affirm wants to build out a more robust offering for its consumers. Affirm initially started with a typical BNPL offering, but has expanded into offering a virtual card (like a credit card essentially), a marketplace personalized for your interests with your data where you can shop and find new products, and finally a savings account. Affirm might be using its BNPL product solely as a customer acquisition tool which will feed the other products and services built on top of that offering such as a savings account.

Total Addressable Market

How large is this market?

Affirm competes in the massive e-commerce market and is even looking to expand both globally and into the broader retail commerce market with its debit card. The size of the market isn’t a big concern for me. Just think of the size of the e-commerce industry + regular commerce both in the United States and abroad.

Affirm pegs the total U.S. retail market at more than $5.0 trillion, Affirm’s take rate (merchant network revenue/GMV) is ~5.0%. 5% of $5 trillion is more than $250 billion. Then there’s also additional upside through other revenue lines like interest income or other products that Affirm currently offers or will offer in the future. All in all, the market size isn’t a concern, rather how much of this accrues to BNPL competitors and more specifically Affirm.

How much can Affirm capture?

The question isn’t how big this market opportunity is, but rather how much can Affirm capture. This is still a competitive market and not a winner take all market. This question depends on a couple of factors. First, how many consumers will use a BNPL product and how much will they spend with a BNPL product?

Competitive Advantages

Network effects?

I think there might be a small network effect within this industry. For example, the more consumers that use Affirm, the more like merchants will take Affirm as the main BNPL offering. I don’t think this is a complete winner take all market, but I do think the top players in this industry will have competitive advantages over smaller competitors looking to disrupt the space.

If anything, I think this space will end up being quite similar to credit card payment rails (Visa, Mastercard, Amex, and Discover). There will likely be a handful of companies that provide the biggest value proposition to consumers and merchants. Right now, the four appear to be Klarna, Afterpay, Affirm, and Paypal.

Sticky platform?

Affirm is building products that go beyond the BNPL space. Most interesting to me is that Affirm has launched a quasi-marketplace and savings account. What if one day, consumers first place to look for deals is the website’s of these major BNPL businesses? As of Q3 2021, 30% of Affirm transactions were initiated on through Affirm’s mobile app and website channels. Affirm has also launched a savings account which is likely a sticky service for consumers.

Financials

Affirm has two major revenue lines, merchant network revenue and interest income. Merchant network revenue is the revenue collected from fees paid by merchants. Interest income is self-explanatory. Affirm pays a lot in transaction costs (which is to be expected) and is not GAAP profitable. Transaction costs include the following:

loss on loan purchase commitment

provision for credit losses

funding costs

processing and servicing

Roughly 43% of Affirm’s GMV is non-interest bearing and the rest is interest-bearing loans.

Through Q3 2021

Merchant network revenue = $290,894

Interest income = $222,624

Total other revenue = $95,166

Total revenue = $608,684

Revenue less transaction costs = $283,893

GAAP EBIT = ($229,522)

GMV = $5,808,415

Active customers = 5,364

Transactions per active customer = 2.3

Merchant network revenue / GMV = 5.0%

Merchant network revenue growth = 69.6%

Interest income growth = 61.8%

Other revenue growth = 102.1%

Revenue less transactions / total revenue = 46.6%

GAAP EBIT margin = (37.7%)

2020

Merchant network revenue = $256,752

Interest income = $186,730

Total other revenue = $66,046

Total revenue = $509,528

Revenue less transaction costs = $160,862

GAAP EBIT = ($107,790)

GMV = $4,637,220

Active customers = 3,618

Transactions per active customer = 2.1

Merchant network revenue / GMV = 5.5%

Merchant network revenue growth = 94.0%

Interest income growth = 56.4%

Other revenue growth = 424.2%

Revenue less transactions / total revenue = 31.6%

GAAP EBIT margin = (21.2%)

2019

Merchant network revenue = $132,363

Interest income = $119,404

Total other revenue = $12,600

Total revenue = $264,367

Revenue less transaction costs = $54,395

GAAP EBIT = ($127,441)

GMV = $2,620,059

Active customers = 2,045

Transactions per active customer = 2.0

Merchant network revenue / GMV = 5.1%

Revenue less transactions / total revenue = 20.6%

GAAP EBIT margin = (48.2%)

What’s Interesting

Shopify Partnership

I think the exclusive partnership with Shopify and its merchants is fantastic for Affirm. Shopify has hundreds of thousands of merchants and being able to be the exclusive BNPL provider is a great sign for Affirm.

While some might argue that Affirm had to buy this partnership by offering Shopify equity in Affirm, I do think that Shopify also wants to pick the best company and won’t sacrifice quality for its merchants. While Affirm might collect lower margins from transactions with Shopify merchants, the overall profit pool is likely much higher being on Shopify.

Bezos has a great quote about profit margins and dollars:

“Percentage margins don’t matter. What matters always is dollar margins: the actual dollar amount. Companies are valued not on their percentage margins, but on how many dollars they actually make, and a multiple of that.”

While Affirm’s margins might decrease as a result of this partnership with Shopify and its merchant base, the amount of profit dollars collected will likely be much higher which will give Affirm a higher potential profit pool and lead to more shareholder value (hopefully).

Beyond BNPL

Affirm wants to do much more than just offer consumers and merchants a BNPL product. Affirm (alongside the rest of the fintech industry) wants to be the primary destination for consumers to shop, save, and process other financial transactions. If Affirm can continue to expand its financial products and build an increasingly sticky platform for consumers and merchants, then Affirm’s competitive advantage looks a lot more attractive to me.

One of the caveats to this is that there are a lot of fintech companies that want to be the primary home for your financial transactions (saving, spending, investing, etc.). This is likely a competitive and saturated strategy, but the rewards might be worth it.

Future Questions

Stronger competitive advantages

I like my companies to have a strong sustainable and growing competitive advantage either currently or in the near-term. I don’t see what Affirm’s sustainable competitive advantage is currently or how strong this competitive advantage truly is. I think the Shopify partnership is a major advantage, but there are also merchants off the Shopify platform which Affirm still needs to win. I’ll likely learn more about some of the major differentiations between Affirm, Afterpay, and Klarna as I do more research on this space, but I don’t see any major green flags that make Affirm stand out for me.

Competition from incumbents

There’s lots of talk about incumbent companies in this space. Besides competition with Klarna and Afterpay, Affirm also faces risks from Paypal, traditional banks and credit card companies.

I think the biggest risk is both other BNPL competitors and Paypal. Paypal has a massive distribution with consumers and merchants and easily make BNPL a feature rather than a whole other company. Other BNPL competitors are also a concern.

The downside for incumbents is that they’d be cannibalizing their own business if they offer a BNPL product. Many of the incumbents’ business models revolve around collecting interest, charging late fees, and other fees that BNPL companies do not charge. BNPL companies are likely more aligned with consumers because these costs are subsidized by merchant fees.

Conclusion

I think the BNPL space is rather interesting, I’m looking forward to learning more. I still have some questions about the industry and some of the competitive factors, but I like what I’m reading from my initial research.

If you’ve enjoyed this edition of Weekly 10-K please considering subscribing, sharing it with friends and colleagues, and following me on Twitter.