#024 - Auto1 Group

#024 - Auto1 Group

Leading European online used car retailer.

Auto1 Group - (ETR: AG1)

Auto1 Group is a leading European online used car retailer. Auto1 Group built its wholesale platform for professional dealers and is looking to build out its retail platform for consumers.

If you enjoy this, sign up for more shallow dives here!

Please note that this article does not constitute investment advice in any form. This article is not a research report and is not intended to serve as the basis for any investment decision. All investments involve risk and the past performance of a security or financial product does not guarantee future returns. Investors have to conduct their own research before conducting any transaction. There is always the risk of losing parts or all of your money when you invest in securities or other financial products.

Industry Overview

The European used car industry is similar to that of the United States. While there are some differences between the United States and European markets, I think the core idea that people will always buy and sell used cars is true.

It’s also unlikely that an American competitor would be able to compete in Europe. The same factors that give Carvana and CarMax an advantage in the United States are the reasons these companies can’t and likely won’t compete in Europe. Sure, CarMax, Carvana, and others might try to expand into Canada or Mexico, but moving across the Atlantic Ocean is an unlikely endeavor. Entering Europe would require extensive infrastructure and a large supply of cars which would be expensive and likely not worth it for those companies currently.

While there are other European online used car retailers, Auto1 Group seems to be the leading company. It does have competition which I will likely cover in the future. The most notable competitor is Cazoo which will list in the US via a SPAC.

Business Overview

Auto1 Group is a European online used car retailer. The companies I’ve previously written about all operate primarily in the United States. Auto1 Group seems to be the leading online used car retailer in Europe.

Auto1 Group has two distinct business lines, “AUTO1” which is Europe’s largest wholesale platform for used cars. More recently, Auto1 Group has launched “Autohero” which is a retail brand for regular consumers to buy used cars. The image below gives a small depiction of Auto1 Group’s business model.

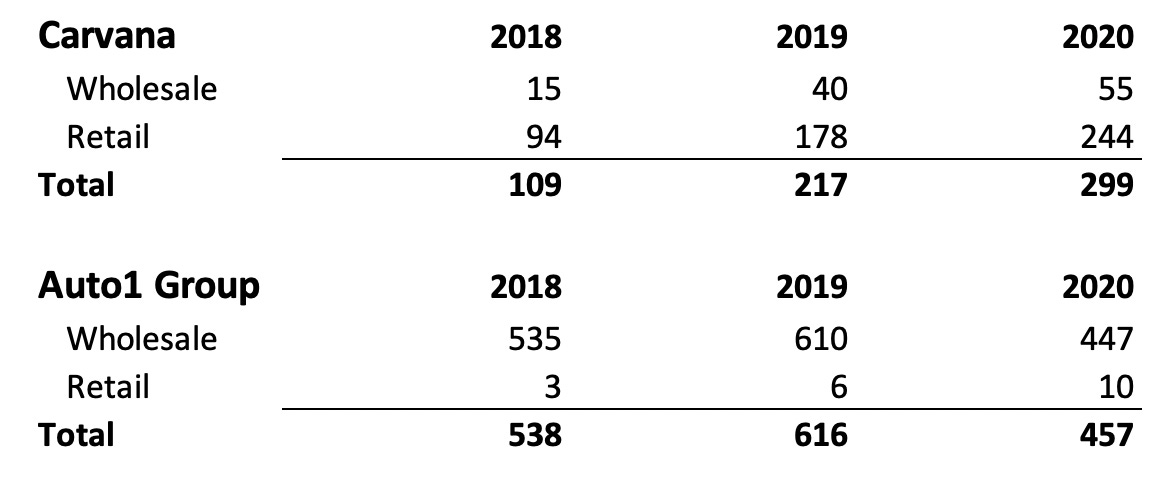

Auto1 Group is able to choose whether or not a car should be sold wholesale or through retail. While most competitors have this option, Auto1 Group benefits even more because of the number of cars it sells through its wholesale platform. For example, in 2020 Auto1 Group sold more than 1.8x the number of cars via its wholesale platform than Carvana’s total retail unit sales in 2020. The image below is just a rough comparison of units sold between Carvana and Auto1 Group.

The other interesting part of Auto1 Group’s wholesale platform is that it had a gross profit margin of more than 10.0% in 2020, whereas Carvana’s used vehicle gross profit margin was 7.6%! If Auto1 Group has better profit margins than Carvana’s used retail car business, does that mean Auto1 Group will have a higher profit margin on its retail business line in a number of years? While the wholesale business likely does not involve the same number of costs as selling a vehicle through a retail sales channel, it is impressive that Auto1 Group has consistently high gross margins on the wholesale business.

How does Auto1 Group make a better profit margin on selling wholesale cars than Carvana makes on selling its own inventory of cars?

Most American competitors don’t have a positive profit margin for the wholesale side of the business. From reading about other companies, most competitors use the wholesale side of the business to control inventory and be able to offload vehicles for a chance of making a small profit. Wholesale for other companies is a cost center, not a profit center. This is a key question that I will likely focus on through the rest of this shallow dive.

Auto1 Group also intends to invest in its Autohero platform which is relatively new and only sold 6,000 cars in 2019 and 10,000 cars in 2020 through the COVID-19 pandemic. This business is relatively immaterial for Auto1 Group today, but the potential is there. I think the potential for Auto1 Group is having both a leadership position as the main wholesale vehicle platform for Europe and being the main online used car retailer of Europe. Auto1 Group might have a better chance of being the leading online used car retailer for a specific geography than Carvana or any of its peers.

Total Addressable Market

Europe’s used car industry is also a massive industry just like the United States. Most estimates have the European used car market valued at more than €600 billion. This is in line with the American used car market. This isn’t a surprise to me and seems to make sense. There are also additional factors such as used car financing that bring this industry size up even more.

Auto1 Group boasts a total addressable market of more than €700 billion when including the financing associated with buying a used vehicle. I think the used car market is massive no matter what country or region you’re looking at. Cars are a necessity in many parts of the world.

Competitive Advantages

Scale

I’ve been including this in seemingly every shallow dive I’ve done in this industry, but I do think it’s likely the most important. I think scale affords companies the ability to offer more competitive prices to consumers, reach more consumers, and have better profit margins. Having scale includes having the ability to deliver vehicles to consumers, to pick up vehicles from dealers or consumers, being able to source the best inventory, and many other important factors. Scale also allows companies to potentially have pricing power over suppliers and other stakeholders in an industry value chain.

Auto1 Group seems to be the leading online used car retailer operating in Europe.

Brand

I’ve touched on this in a number of the shallow dives I’ve completed on various competitors, but I think consumers want a trustworthy and recognizable brand when buying a used car. Used cars are an expensive and important purchase for consumers. If Auto1 Group is the leading destination to both buy and sell a car, it seems as though it likely has advantages over incumbents and other peers.

I don’t think brand alone would give Auto1 Group a competitive advantage, but I do think that it’s an important factor that would be hard to overcome when Auto1 Group likely also benefits from scale. Hard to be known by all consumers when you don’t have the scale necessary to serve all countries or all parts of a continent.

Financials

All of the following figures are in millions and euros (unless otherwise stated).

2020

Merchant business line (Auto1)

C2B revenue = 2,349

Remarketing revenue = 348

Gross profit = 283

Cars sold through C2B (in thousands) = 397

Cars sold through remarketing (in thousands) = 50

Gross profit per unit = 633

C2B revenue growth = -24.4%

Remarketing revenue growth = 20.7%

Gross profit margin = 10.5%

Retail business line (Autohero)

Retail revenue = 133

Gross profit = 3

Cars sold (in thousands) = 10

Gross profit per unit = 285

Revenue growth = 62.9%

Gross profit margin = 2.2%

2019

Merchant business line (Auto1)

C2B revenue = 3,106

Remarketing revenue = 289

Gross profit = 341

Cars sold through C2B (in thousands) = 571

Cars sold through remarketing (in thousands) = 39

Gross profit per unit = 559

C2B revenue growth = 17.0%

Remarketing revenue growth = 73.5%

Gross profit margin = 10.0%

Retail business line (Autohero)

Retail revenue = 81

Gross profit = 1

Cars sold (in thousands) = 6

Gross profit per unit = 254

Revenue growth = 154.4%

Gross profit margin = 1.8%

2018

Merchant business line (Auto1)

C2B revenue = 2,654

Remarketing revenue = 166

Gross profit = 242

Cars sold through C2B (in thousands) = 515

Cars sold through remarketing (in thousands) = 20

Gross profit per unit = 452

C2B revenue growth = 28.0%

Remarketing revenue growth = 66.4%

Gross profit margin = 8.6%

Retail business line (Autohero)

Retail revenue = 32

Gross profit = 0

Cars sold (in thousands) = 3

Gross profit per unit = 0

Revenue growth = 788.9%

Gross profit margin = 0.0%

Don’t be fooled by the high growth in the retail business for Auto1 Group. This is a tiny base of revenue and high growth rates should be expected. I’m also not concerned with the low gross margins from the retail business as Auto1 Group scales and is able to have better economies of scale as this business progresses.

What’s Interesting

Wholesale platform before retail platform?

I’m most curious about Auto1 Group’s core business which is the wholesale platform for buying and selling used cars. Why did Auto1 Group start off with this strategy? What does this mean for its business and its ability to build out a core retail business for consumers? Does this wholesale business give Auto1 Group an advantage in choosing which cars should be sold retail to consumers?

Growing retail platform

This is where Auto1 Group’s future potential and growth probably lies. While only 10,000 cars were sold through its retail business line (Autohero), there is likely an obvious path to selling more than 100,000 cars in potentially a number of years? I think looking to more mature American competitors with a scaled retail platform is an easy comparison and also likely the best comparison. Carvana sold more than 244,000 retail units in 2020. I’d say it’s quite likely that Auto1 Group can reach even a quarter of these units in a number of years.

Future Questions

What are the major differences between US and European used car retailers?

There’s obviously going to be some major differences between the way people use cars based on just broad societal differences between Europe and the US. There are likely some differences on the total number of cars per person in the US and in Europe. This might just be a minor question or concern, but this is something I’d want to double check.

Auto1 Group offer financing solutions?

Auto1 Group works with 3rd party companies to offer consumers financing options. Other similar companies like Carvana and CarMax use in-house financing (with some slight differences) to offer consumers financing options. I’m surprised with Auto1 Group’s current size it doesn’t offer in-house financing for consumers and continues to rely on 3rd parties, especially when considering the profitability of this opportunity (but there are also risks associated with this).

Wholesale business?

What’s up with the massive wholesale business? No competitors or peers even come close to having a wholesale business the size of Auto1 Group. Auto1 Group is also able to make a consistent positive gross profit margin. While this might just be a result of scale, it’s still impressive that Auto1 Group has been able to do this consistently and no other company has. I would want to learn more about this piece of the business. It sounds as though Auto1 Group controls the value chain from the minute it picks up the car from a dealer (remarketing) or from a consumer (C2B) and sells it to a dealer. Therefore Auto1 Group doesn’t have to worry about paying auction fees or other middlemen that would take away from a low profit pool.

Conclusion

I think Auto1 Group is a really interesting business and I wish it got more coverage from investors. I think there’s a lot to learn from this business that could possibly be applied to its US peers. I think if you’re bullish on this space but don’t like Carvana (for obvious reasons) and you don’t like any other American companies, Auto1 Group might be a fine option for you.

You should always do your own work. This shallow dive is only meant as an introduction to the company.

If you’ve enjoyed this edition of Weekly 10-K please considering subscribing below, sharing it with friends and colleagues, or following me on Twitter.